WorldQuant alphas

Terms

Alpha testing parameters

Universe

-- Subset of stocks ranked by liquidity. Smaller = more liquid

* Includes TOP3000, TOP2000, TOP1000, TOP500, TOP200

Delay

-- Data delay

* Delay = 1 alphas trade in the morning using data from yesterday

* Delay = 0 alphas trade in the evening using data from today

* Delay 0 alphas perform better, so they have harder submission requirements

Neutralization

-- Adjust alpha weights to sum to zero within each group of the selected type

* Includes Market, Sector, Industry, Subindustry, or Non

Alpha performance metrics

Sharpe

`Sharpe` -- Average measure of risk-adjusted returns

* Sharpe = Avg. Annualized Returns / Annualized Std. Dev. of Returns

Turnover

`Turnover` -- Average measure of daily trading activity

* Turnover = Value Traded / Value Held

Fitness

`Fitness` -- Hybrid metric for overall performance. Higher is better.

* Fitness = Sharpe * Sqrt( Abs( Returns ) / Max( Turnover, 0.125 ) )

Returns

`Returns` -- Annualized average gain or loss as a fraction of the invested amount.

* Invested amount is equal to half the book size

Margin

`Margin` -- Average gain or loss per dollar traded

* PnL divided by total dollars traded in a given time period

Operators

Operators are building blocks

* each one has a detailed explanation/math definition

* add, subtract, mult, div -- be aware of units!

* if/else, ternary

* logical and, or, not

* less/greater comparisons, eq/neq

Cross-sectional operators perform op across all stocks in universe at given point in time

* rank, zscore, scale, sign

Time-series operators perform op on one stock across many points in time

* tsdelta, tsdelay, tssum, tsmean, tsrank, tszscore, tsstddev, tsregression

Group operators are more powerful cross-sectional operators

* Pick group like sector, industry, subindustry

Time-series regression

* tsregression(y, x, window, lag, retval) -- y(t) = a + b * x(t-lag) for t in past window days. Returns error, a, b, estimate.

Cannot do cross-sectional correlation, only time-series correlation

Tradewhen operator activates between entry and exit conditions

* Reduces turnover

* Useful for trading during high-volatility times

Humpdecay -- return today's or yesterday's price, depending if change exceeds hump value

* Reduces turnover

Good values

* Truncation value = 0.01 for diversity

* Reversion threshold = 0.55 because research show 50% time reversion, 10% momentum, 40% random

Price-Volume alpha

Ideas

Trend reversion

* Short overbought stocks, buy cheap stocks

* Useful in long-short frameworks

* Works well during extreme price movements (overreaction)

* Consider stddev to measure extreme price movements

* Trade during times of high volatility

Try alpha `-(close - ts_mean(close, 5))`

* Revert to weekly price, compared cross-sectionally

* Uses absolute difference, so high prices are unfairly up-weighted

* Long-short neutralization is performed to balance long and short positions

* Wrap alpha with `rank` operator to get percentile? Helps with weighting

* Good trick to improve diversity and performance

Reduce turnover = percent of portfolio traded per day ~ transaction costs!

* Increase alpha decay

* Combine operators

* Also reduces correlation

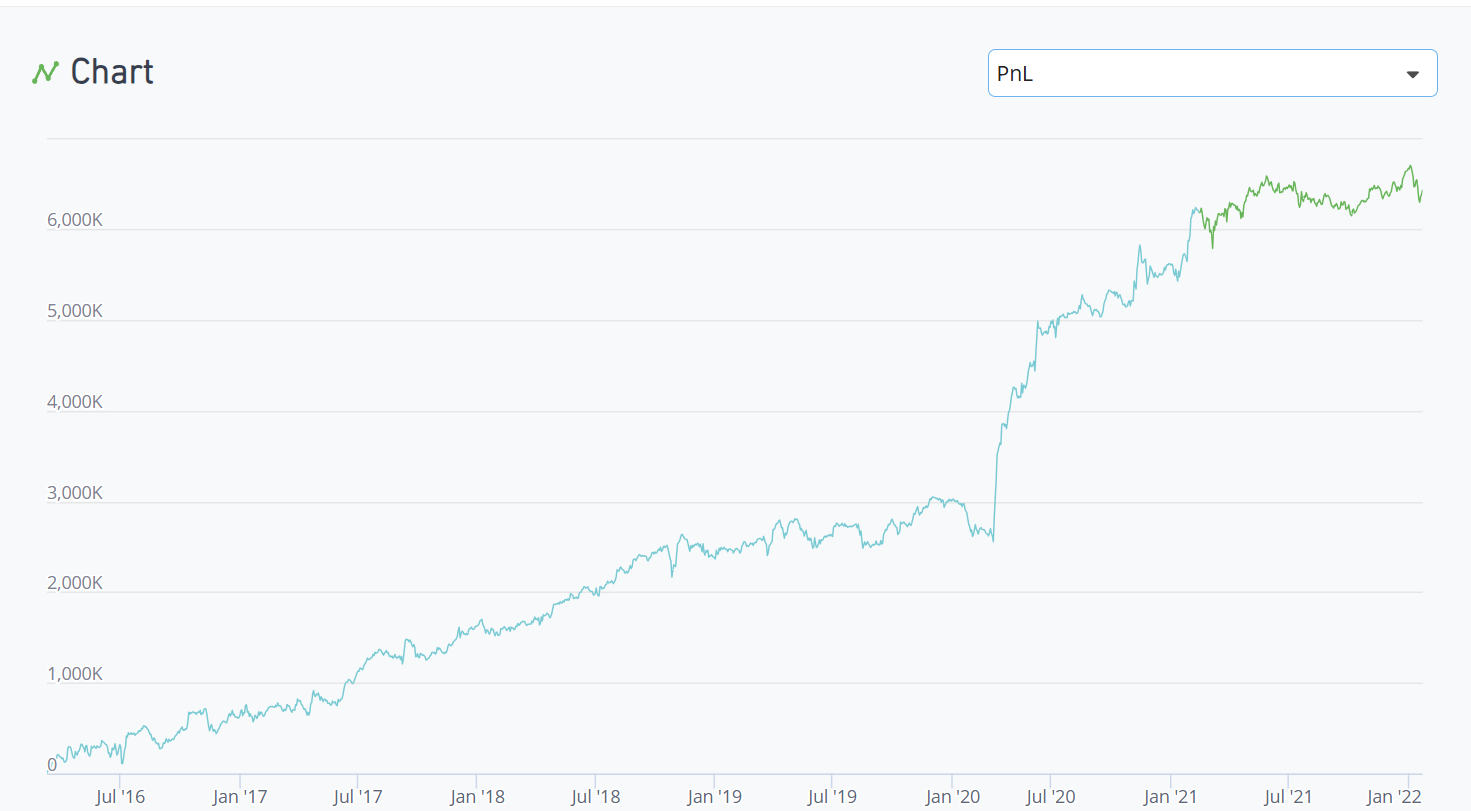

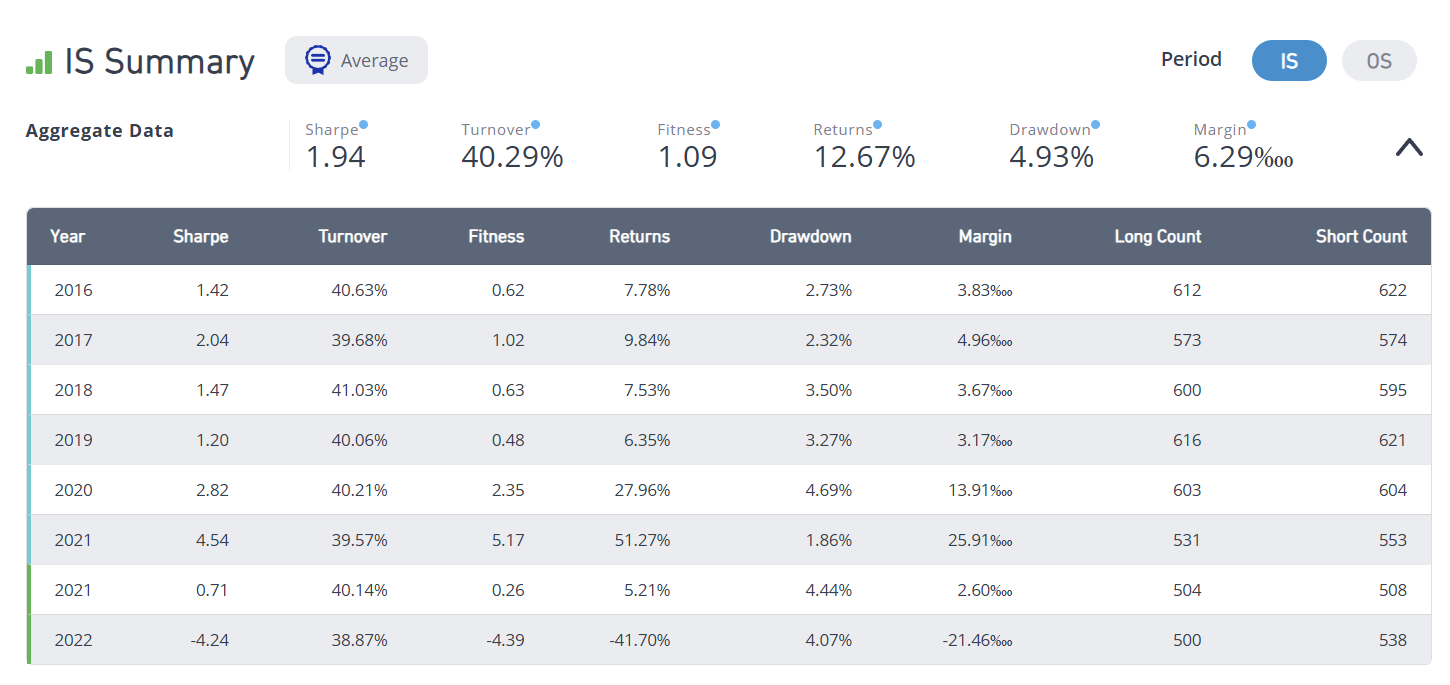

example

summary